Do you go through underwriting twice?

These days, many lenders are required to check the borrower's credit twice during the home loan application process: once during pre-approval and once right before closing.

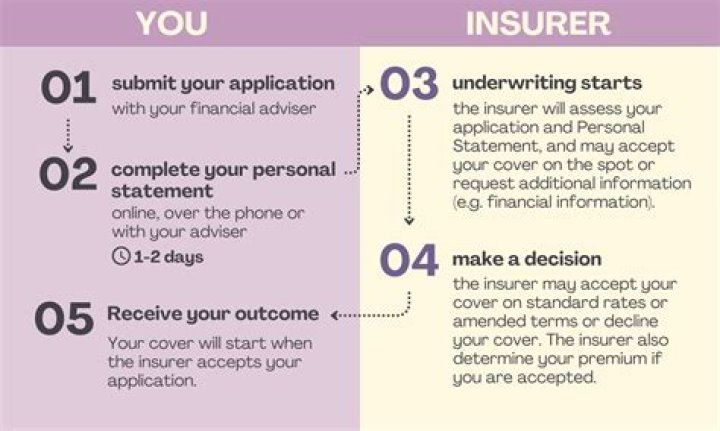

Does underwriting happen twice?

The short answer is that it takes place somewhere in the middle of the process. It happens after the loan application has been completed, and before the final approval and funding.Does the underwriter make the final decision?

Mortgage underwriting is the process through which your lender verifies your eligibility for a home loan. The underwriter also ensures your property meets the loan's standards. Underwriters are the final decision-makers as to whether or not your loan is approved.How often do you get denied in underwriting?

Mortgage underwriters deny about one in every 10 mortgage loan applications. This is often because the applicant has too much debt, a spotty employment history, or a low appraisal report. However, by knowing what an underwriter reviews, you can make your application as attractive as possible.Can you be denied after underwriting?

Your loan is never fully approved until the underwriter confirms that you are able to pay back the loan. Underwriters can deny your loan application for several reasons, from minor to major. Some of the minor reasons that your underwriting is denied for are easily fixable and can get your loan process back on track.How long does it take for the underwriter to make a decision?

Is no news good news in underwriting?

When it comes to mortgage lending, no news isn't necessarily good news. Particularly in today's economic climate, many lenders are struggling to meet closing deadlines, but don't readily offer up that information. When they finally do, it's often late in the process, which can put borrowers in real jeopardy.What are red flags for underwriters?

Red flags for underwriters are issues that arise during processing and are questionable. Different types of underwriters have their red flags to look out for, but in general, underwriters are tasked to find suspicious discrepancies in applications to better assess financial risks.What should you not do during underwriting?

Tip #1: Don't Apply For Any New Credit Lines During Underwriting. Any major financial changes and spending can cause problems during the underwriting process. New lines of credit or loans could interrupt this process. Also, avoid making any purchases that could decrease your assets.How often do underwriters deny FHA loans?

You may be wondering how often underwriters denies loans? According to the mortgage data firm HSH.com, about 8% of mortgage applications are denied, though denial rates vary by location and loan type. For example, FHA loans have different requirements that may make getting the loan easier than other loan types.Do underwriters look at spending habits?

Lenders look at various aspects of your spending habits before making a decision. First, they'll take the time to evaluate your recurring expenses. In addition to looking at the way you spend your money each month, lenders will check for any outstanding debts and add up the total monthly payments.How long after underwriting is closing?

Final Underwriting And Clear To Close: At Least 3 DaysOnce the underwriter has determined that your loan is fit for approval, you'll be cleared to close. At this point, you'll receive a Closing Disclosure.

What comes after underwriting?

What Happens After my Mortgage Loan is Underwritten? Once your loan goes through underwriting, you'll either receive final approval and be clear to close, be required to provide more information (this is referred to as “decision pending”), or your loan application may be denied.How do I know if my mortgage will be approved?

You'll have the best chances at mortgage approval if:

- Your credit score is above 620.

- You have a down payment of 3-5% or more.

- Your existing debts are low.

- You've had a stable job and income for at least two years.