How close do underwriters look at bank statements?

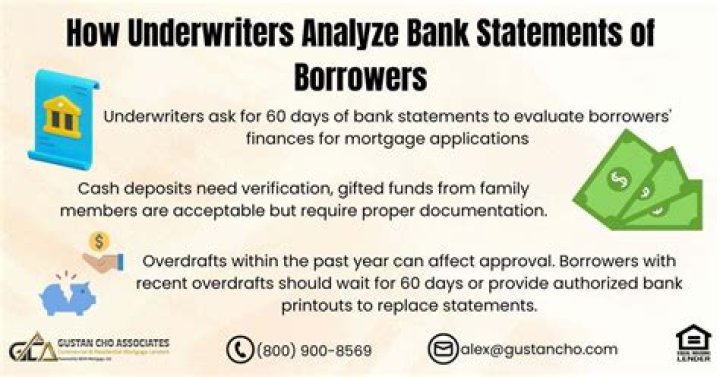

How far back do mortgage lenders look at bank statements? Generally, mortgage lenders require the last 60 days of bank statements. To learn more about the documentation required to apply for a home loan, contact a loan officer today.

How many months of bank statements do underwriters look at?

During your home loan process, lenders typically look at two months of recent bank statements. You need to provide bank statements for any accounts holding funds you'll use to qualify for the loan, including money market, checking, and savings accounts.Do underwriters check bank statements before closing?

Yes, they do. One of the final and most important steps toward closing on your new home mortgage is to produce bank statements showing enough money in your account to cover your down payment, closing costs, and reserves if required.Do underwriters verify bank statements?

Once underwriting is complete, your lender will tell you whether or not you qualify for a home loan. Here are a few red flags that underwriters look for when they check your bank statements during the loan approval process.Can bank statements stop you getting a mortgage?

Mortgage lenders require you to provide them with recent statements from any account with readily available funds, such as a checking or savings account. In fact, they'll likely ask for documentation for any and all accounts that hold monetary assets.Bank Statements for Mortgage - What do Underwriters Look For?

How far back do mortgage lenders look at bank statements?

How far back do mortgage lenders look at bank statements? Generally, mortgage lenders require the last 60 days of bank statements. To learn more about the documentation required to apply for a home loan, contact a loan officer today.How far back do mortgage lenders look?

How far back do mortgage credit checks go? Mortgage lenders will typically assess the last six years of the applicant's credit history for any issues.Do lenders look at spending habits?

Lenders look at various aspects of your spending habits before making a decision. First, they'll take the time to evaluate your recurring expenses. In addition to looking at the way you spend your money each month, lenders will check for any outstanding debts and add up the total monthly payments.How are bank statements verified?

The borrower has to provide the lender with the two most recent bank statements to confirm they have enough money for a downpayment. The mortgage company then reaches out to the borrower's bank to verify if the information available on the bank statement is authentic or not.How often does an underwriter deny a loan?

Mortgage underwriters deny about one in every 10 mortgage loan applications. This is often because the applicant has too much debt, a spotty employment history, or a low appraisal report. However, by knowing what an underwriter reviews, you can make your application as attractive as possible.What are red flags for underwriters?

Red flags for underwriters are issues that arise during processing and are questionable. Different types of underwriters have their red flags to look out for, but in general, underwriters are tasked to find suspicious discrepancies in applications to better assess financial risks.Do underwriters look at overdrafts?

One area mortgage underwriters look for is when bank accounts go negative. This is called an overdraft or nonsufficient funds (NSF). An overdraft is when the account goes negative, but the debit or check is covered. Conversely, an NSF is not covered and an example is a bounced check.Can my loan be denied at closing?

Can a mortgage loan be denied after closing? Though it's rare, a mortgage can be denied after the borrower signs the closing papers. For example, in some states, the bank can fund the loan after the borrower closes. “It's not unheard of that before the funds are transferred, it could fall apart,” Rueth said.How long does it take for underwriter to clear to close?

Final Underwriting And Clear To Close: At Least 3 DaysOnce the underwriter has determined that your loan is fit for approval, you'll be cleared to close. At this point, you'll receive a Closing Disclosure.