What is the COSO model?

The COSO Framework is a system used to establish internal controls to be integrated into business processes. Collectively, these controls provide reasonable assurance that the organization is operating ethically, transparently and in accordance with established industry standards.

What are the 5 elements of COSO?

The 5 Components of COSO: C.R.I.M.E. The five components of COSO – control environment, risk assessment, information and communication, monitoring activities, and existing control activities – are often referred to by the acronym C.R.I.M.E.Why is the COSO framework important?

The overarching goal of a COSO Framework is to enhance and improve organizational performance and oversight, as well as reducing the extent of the risk of fraud.What are COSO control activities?

Control activities are one of the key components of the COSO internal control framework. Control activities are actions (generally described in policies, procedures, and standards) that help management mitigate risks in order to ensure the achievement of objectives.What is COSO mapping?

COSO Mapping and TemplateAt A2Q2, we have created a COSO mapping template where a company can match key SOX controls to each component, principle, and point of focus. The template clearly shows if a gap exists.

Internal Control | COSO Framework

What is COSO risk assessment?

Risk AssessmentCOSO advocates for identifying and analyzing risks that may adversely affect the achievement of an objective and risks that may positively affect the objective. To ensure a clear risk assessment, the organization should specify the objectives and outline the risk in each stage.

How does COSO define internal control?

The COSO model defines internal control as “a process effected by an entity's board of directors, management and other personnel designed to provide reasonable assurance of the achievement of objectives in the following categories: Operational Effectiveness and Efficiency.Who uses COSO framework?

COSO is a committee composed of representatives from five organizations: American Accounting Association. American Institute of Certified Public Accountants. Financial Executives International.What are the 3 COSO internal control objectives?

Conclusion. COSO objectives refer to the company's goals. These objectives are broken into three areas operations, reporting, and compliance. Management must have a vision for the company's objectives they want to achieve before designing the internal control system.Why COSO is important in internal control?

According to the COSO board, the updated framework offers companies more effective internal controls, which will allow organizations to better mitigate risks and have the data necessary to support sound decision-making.Why is COSO three dimensional?

GOING BACK TO ITS ORIGINAL 1992 release, the COSO internal control framework was always meant to be viewed as a three-dimensional model or framework, where each cell component in any one dimension was meant to have a relationship with corresponding cells in the other two dimensions.How is COSO used in internal audit?

The four principles of the COSO risk assessment component are:

- Specify appropriate objectives,

- Identify and analyze risks,

- Evaluate fraud risks, and.

- Identify and analyze changes that could significantly affect internal controls.

Is COSO a regulation?

Because COSO's Internal Control—Integrated Framework is a framework, not a regulation or requirement, a COSO audit, by definition, doesn't exist. However, the COSO framework is very useful for achieving compliance with the Sarbanes-Oxley Act (SOX), which federal law requires for all publicly traded companies.How many principles are present in the COSO framework?

COSO Framework's 17 Principles of Effective Internal Control.Why was COSO created?

COSO was formed in 1985 to sponsor the National Commission on Fraudulent Financial Reporting, an independent private-sector initiative which studied the causal factors that can lead to fraudulent financial reporting.What are the steps in COSO risk monitoring?

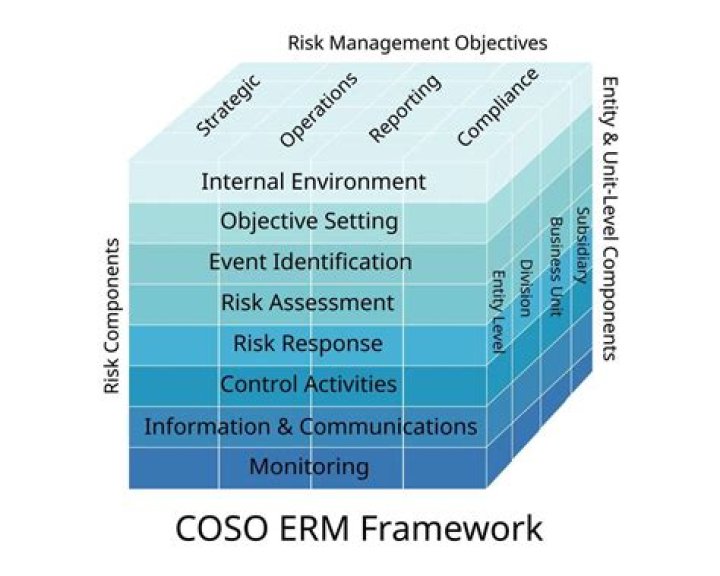

- Internal environment. The internal environment establishes the tone of the organisation, influencing risk appetite, attitudes towards risk management and ethical values. ...

- Objective setting. ...

- Event identification. ...

- Risk assessment. ...

- Risk response. ...

- Control activities. ...

- Information and communication. ...

- Monitoring.